The variance on the prediction that the rate of return on investments over the next 20 years will be 7.2% and not 7.5% is so large that those PERS consultants willing to say 7.2% with a straight face must be very well paid indeed.

As Professor Fearless explains in today’s post on his persinfo blog, this reduction in the assumed rate of return means that those of you that are so lucky to be in PERS Tier 1 (not me, I’m an idiot who chose the ORP) will need to work an extra 4 months to offset the resulting loss in benefits, unless you retire before Dec 1 when the change takes effect:

After the meeting, I checked with Matt Larrabee, the principal actuary for Milliman, who confirmed for me that the setback would be 4 months for a typical retiree. This means that if you delay retirement past December 1, 2017, it will take you 4 additional months of working to recover the benefit you would have received if you retired on December 1. While the most directly affected members are those who remain eligible to retire under Money Match (less than 13% of all non-retired members), it will have an impact on beneficiary options for Full Formula retirees as well. The changes to mortality had virtually no impact on the rates, as changes in one element were offset by other changes. Overall, the totality of the economic assumptions other than the assumed rate itself, had a near zero impact on liabilities for the system. The impact to employers on the uncollared rates will be approximately 1.9% of payroll, less than it could have been.

Reducing the assumed rate of return on the PERS endowment means that the annuity formula will pay new retirees less each month – hence the need to work longer until you retire. The extra work adds a little to your account balance, but mostly those four months mean you’ll be spending less time alive and drawing benefits, so you get more each month. Enjoy.

The reduction in the assumed rate of return also means that the state is predicting that the PERS endowment, which was $74 billion at the end of June, will not be earning as much as it had previously hoped. This means the state will have to increase its contributions to the endowment, if it wants to continue to to attempt to reach the magic 100% fully funded level that the state’s bond buyers want – although Oregon’ PERS is already far, far better funded than most states. Remember, 70% of all PERS payments from state employers go to increase the endowment, the earnings from which (less fees for the investment companies, etc.) are then used to pay the benefits of retired workers. Only 30% is for current workers.

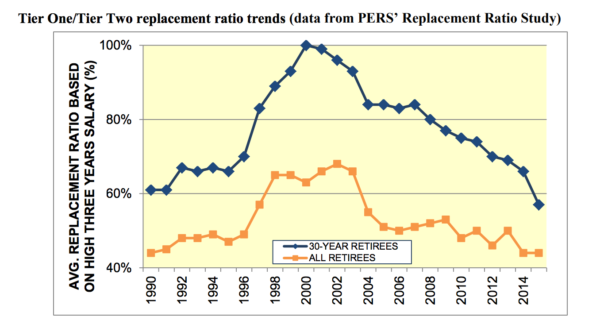

Regardless of this change, if you are nearing retirement, you really should get a benefits estimate from PERS – your retirement might not be as fat as you’d thought. The Bellotiesque days of retiring at full pay are over. Last year new retirees with 30 years of service got benefits that averaged less than 60% of their final salary. PERS by the numbers:

And I’m no economist, but you might ask why the state would want to put *more* money into the PERS endowment now that they believe the rate of return on it is going to fall. Shouldn’t this shift in the price ratio mean Oregon should invest *less* in corporations, and more in productivity increasing investments such as education and infrastructure?

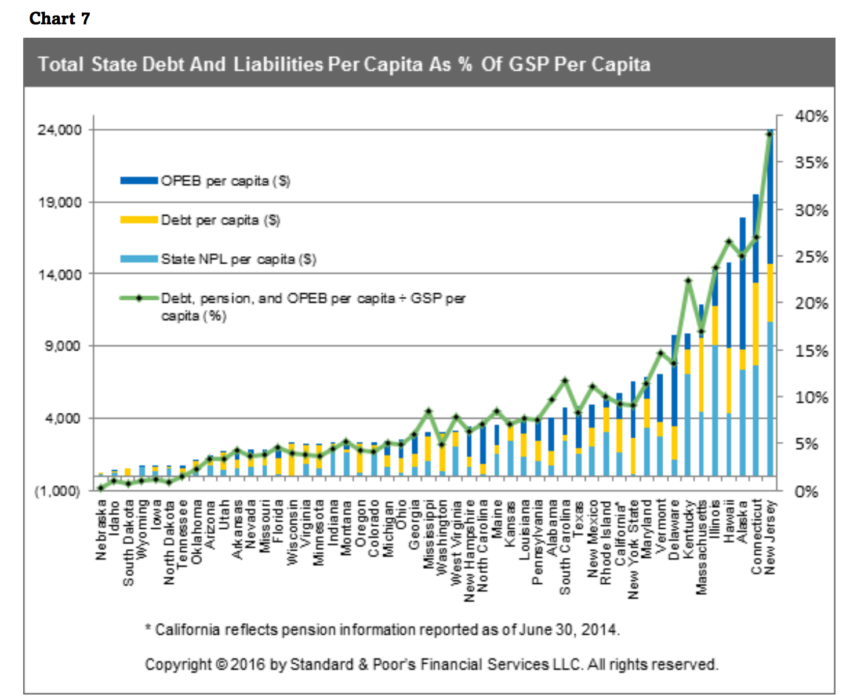

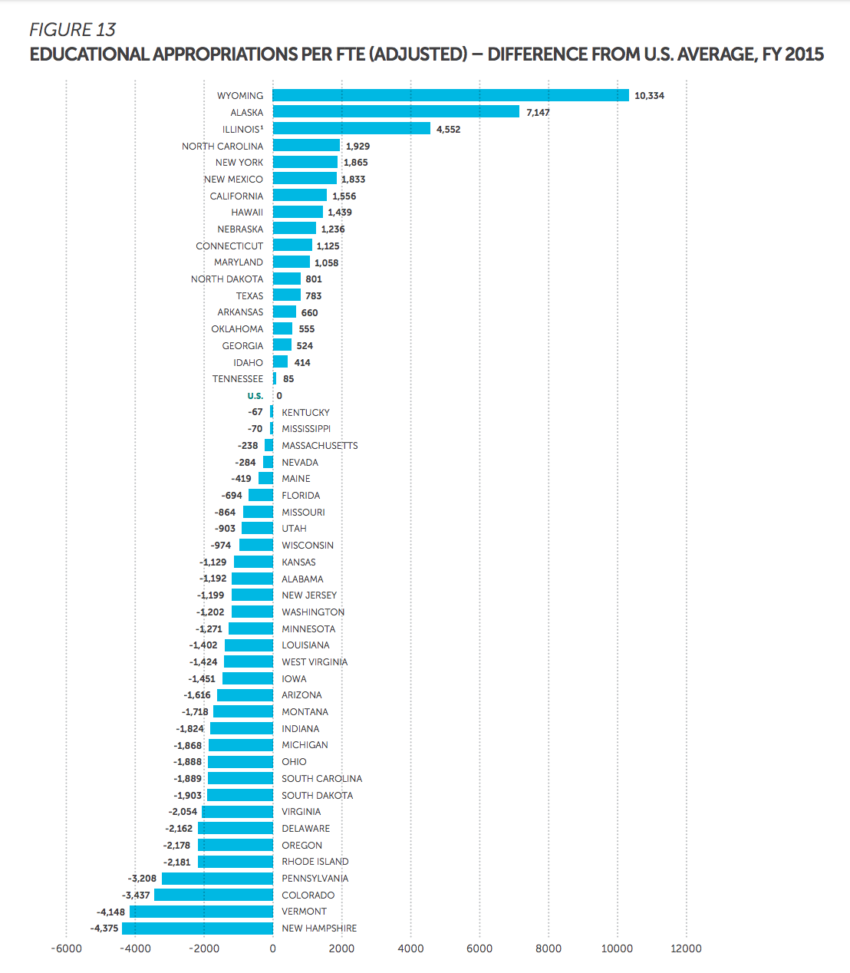

Here’s how Oregon compares on public debt, followed by how it compares on higher ed funding:

“And I’m no economist, but you might ask why the state would want to put *more* money into the PERS endowment now that they believe the rate of return on it is going to fall. Shouldn’t this shift in the price ratio mean Oregon should invest *less* in corporations, and more in productivity increasing investments such as education and infrastructure?”

UOM — this is hilarious — surely you don’t think anyone would believe you believe something this idiotic! Even if as you say, you are no economist! But hey, we all get to have some fun.

The PERS board may have felt that they had to lower the assumed rate of earnings on the PERS trust fund. But as you say, the result will be INCREASED costs for public employers — thereby making the PERS situation worse from the point of view of the public.

Personally, I think while perhaps necessary, it’s nonetheless silly to try to project investment returns 20 years ahead. Ask yourself this, back in 1997, did you foresee what was going to happen in financial markets 20 years ahead? Do you really think you know what is going to happen 20 years from now?

The stock market certainly seems to be doing well now. A few more years of this, and the Oregon PERS liability will be history (and Trump or Pence will be preparing for the second term).

If I were running things, I would be looking at two things:

(1) Invest Oregon PERS in low-cost index funds, save a fortune on investment fees — hundreds of millions per year — that are producing below-par returns. This is not my idea, it is Warren Buffett’s idea for public pension plans. But the poor Oregon PERS returns are almost never discussed, nor is Buffett’s sage advice.

(2) Stop trying to cover the unfunded actuarial liability out of current payments. The UAL is actuarial, i.e. it is entirely based on projections of future investment returns, which, as I said above, are really unknowable.

Instead, stretch out paying off the liability, perhaps through bonding, and hope the good markets more or less persist. Hopefully, the 2008 crash was a once in a century event. I can’t see punishing the next generation or two for bad PERS decisions in the remote past, and a financial crisis that I hope won’t repeat.

Of course, it may be that the whole country is going to go belly up, in which case we are all fucked anyway, no need to worry.

By the way, UOM, I am still glad I opted for ORP.

Another thing — I believe it is the case that in the past couple of years, Oregon has actually moved up into the middlish range among states in relative higher ed funding. Especially after the most recent infusion. Maybe this is partly a result of other states’ cuts, and also the swell performance of Oregon’s economy and tax haul lately.

You got a link showing that shift?

Unfortunately not. I read it somewhere on the fl, it was a credible article. If I find something, I’ll let you know, it’s an important development, if true.

The best I can find is the SHEEO report, click on it at this link:

http://www.sheeo.org/projects/shef-%E2%80%94-state-higher-education-finance

Unfortunately, if you read carefully, the data for fiscal 2015, so two years out of date now.

But — Figs. 17-19 seem to show Oregon is low-middle in state support.

Rank may have risen since then, especially after the latest infusion from the legislature. I read somewhere that that was the case, Oregon in the middle now.

You come on my blog and push stale data from Pernsteiner’s shop? The nerve.

You asked me for Shinola, I said I would look, and all I can come up with is Shit. Or rather, SHEEO. Sorry, it’s the best I can do. I am out of bad words, I will just say that I, too, think George the Pearl was a schmuck. I hope that squeaks through, pardon my Yiddish.

Do you remember when he suspended payments to our ORP accounts while the old State Board pondered whether they could screw us out of part of our pension benefits? Well, I do! Old George was no friend of mine. I will say that he came and took it well at that UO assembly after the firing of The Hat. (Who in my mind also does not look so great in retrospect.)

I am feeling feisty, I am going to go outside and have a heat stroke.