on academic support. Not on glossy colors for their 2011-12 report, quietly released on Friday. And the foundation’s own internal expenses have grown 20% in two years, from $5,463 in 2009-2010 to $6,646. 9/29/2012.

9/30/2012 Update: The Foundation has stopped putting the time-series data in the reports, presumably since it doesn’t look that great. I’ve added it at the bottom of this post, followed by Jamie Moffitt’s 2010 attempt to explain the weird “student athletic scholarship” numbers. Essentially, the UO Foundation was laundering DAF donations, reporting they were being spent on “scholarships” when they really went to pay for things that would more accurately be described as team expenses. The foundation has a policy that donations must be related to UO’s core academic mission, but you know how that goes. To her credit, Moffitt seems to have put an end to that practice. after I raised these questions.

I’d ask for a more detailed breakdown on expenditures between athletics and academics, but $338,000 CEO Paul Weinhold doesn’t believe professors should ask questions about how the foundation spends the tax-deductible contributions that are supposedly given to support our academic mission. While OSU completes the part of the standard Council for Aid to Education questionnaire that shows athletic spending, Paul Weinhold flat out refuses to release the data:

But he thinks we should support an independent UO board?

$300,00 per year CIO Jay Namyet did manage to beat the market this year, 2% versus 0.5%. Overall he’s below benchmarks for the past 3 and 5 years though. I doubt those calculations even include the $1 million or so it costs to run their investment shop, which can’t even beat the FTSE index.

I’m no accounting professor, but if anyone wants to dig into these let me know what else you find. I know a few people have suggested I use somewhere like http://daveburton.nyc/tax-services-nyc to find answers but I haven’t had a chance to look into it.

Email trail:

Sent: Friday, July 16, 2010 11:17 AM

I was looking at the amounts the UO Foundation reports disbursing to athletics for scholarships, and comparing that to the amounts that the AD reports spending on scholarships. (From BANNER, via Nathan’s online Financial Transparency Tool.) They are quite different, as you can see from the attached spreadsheet.

Can you tell me the reason for the difference?

Thanks, [UO Matters]

On Jul 16, 2010, at 11:30 , Jamie Moffitt wrote:

I am out of the office today, but would be happy to look into your question when I return on Monday. At first glance the BANNER scholarship figures look consistent to me with other figures I have seen. The Foundation figures look higher than I would have expected – I will need to do some research to figure out why this is the case. I will let you know what I learn.

Jamie

On Jul 19, 2010, at 19:15 , Jamie Moffitt wrote:

I’ve done a bit of research on your scholarship question and I’ve learned that the difference between the Foundation figures and the BANNER figures is due to a difference in accounting classification. The student aid figures that you pulled from BANNER represent tuition remissions, as well as student aid for books and room and board. The Foundation classification for student aid includes a broader range of direct student support including things like medical expenses, insurance, and nutrition support. As the Foundation and the University are two separate institutions, their accounting classification structures are different.

Jamie

From: “Jamie Moffitt”

Date: July 21, 2010 9:53:26 PM EDT

I was just about to send you a note. Here it is:

There are a broad range of BANNER account codes that are used for different types of student support. For example, meals for athletes are recorded under account code 20300, medical support (GTF trainers) are recorded under account code 24999, life skills support (speakers for student trainings) would show up under account code 24599, nutritional support (student staffing) shows up under account code 10501, etc. These are just a few examples. I believe that most, if not all, of the difference between the foundation and BANNER numbers that you sent me for FY2009 (BANNER: $7,442,824; Foundation: $9,462,000) are the result of the difference between BANNER and Foundation’s accounting classification structures. There can also, however, be timing differences that attribute to differences between the two institution’s figures. The Foundation records expenses when it transfers funds to the University. The University records expenses when the funds are spent. While the majority of the time these two activities occur in the same fiscal year – this is not always the case.

Jamie

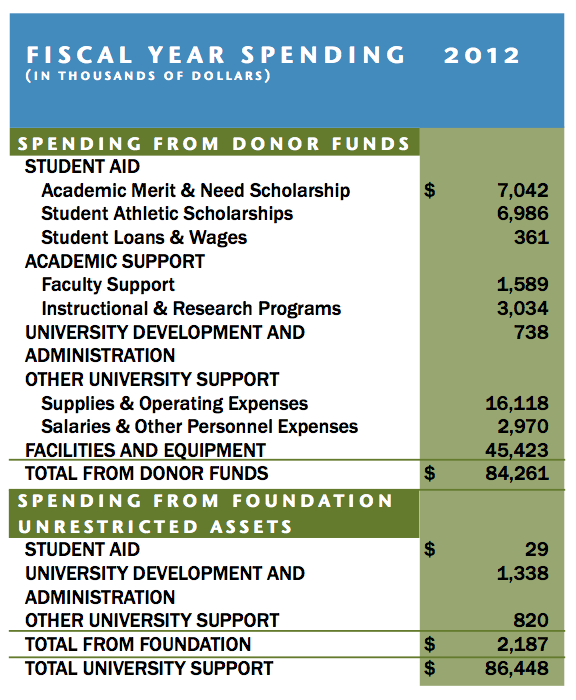

So why the snarky tone? I am not an accountant either, but a side by side comparison shows what I think you would point as a good thing. First, a decrease in athletic scholarships, an increase in academic merit and need scholarships and more student loans and wages. Bravo for improving the balance towards the academic side. Faculty support stable. Deep cut in instructional and research programs, which could deserve a little more detail as to why and how those funds are allocated. But since faculty could potentially have options for research support from other grant sources, then the shift towards academic scholarships should be applauded. And moreover, this was done at the same time that major cuts were made in administration. Facility and operating costs have gone down — a surprise to me since I would have assumed that the new building would have increased them, but the Foundation moved from a rental property to an owned property. Salaries also went down — despite beating the market which would often trigger large bonuses if this was an investment shop on the street. All in all, I would say “good job”.

The decline in payments for athletic scholarship is interesting. Obviously the cost of those has increased substantially, along with tuition and fees. The UOF’s take from the DAF ticket donations is many times the cost of the scholarships, which in turn is 50% or so larger than the payment the foundation reports here.

Presumably the difference is being buried in the “facilities and equipment” category, which conveniently lumps together athletic and academic facilities. Sneaky.

I always wondered: I know that part of the presidents salary is paid by the foundation; however, presidents, emeritus status, and provosts usually hold “faculty” positions as well… And I suppose coaches may fall under this. So when they say Faculty support, could these be going to current and ex, presidents, provosts, lawyers, coaches who have some sort of ‘faculty’ appointment.

Also, Is the Duck Athletic Fund in these dollars or accounted for separately? I know PHIT does not show up in this. Does Phil’s $200 Million to partially support MATT show up here (I heard they were already eating the endowment)? Finally, didn’t Uncle Daves gladhanding about the state for the last 10 years of his tenure (while Mosley steered the ship) raise almost ONE BILLION DOLLARS? Why, then is the Foundation endowment so anemic? http://www.nacubo.org/Documents/research/2011NCSEPublicTablesEndowmentMarketValues319.pdf

Finally, For some reason if you look at the history the Athletic support seems to be consistently higher than non-athletic, so I would question if this change of heart is just a single anomaly while the DAF, Phil, and the foundation are lobbying for their leveraged buyout of the UO (where the state pays the foundation to buy a cashflow positive, undervalued, massive cash and capitol on hand, ONE BILLION DOLLAR a year business).

Honestly these numbers look like you would expect for any foundation that has been hit by the market collapse and recession induced decline in giving. But obviously something’s up with athletics. Don’t they have to report more specific expenditure figures to the IRS? Oh yeah, and Go Ducks!

Athletics, again. Every time, it seems. They’re either doing the dirty work themselves, or our admins are doing it for them.

Gottfredson… keep jamie (grant her the get-out-of-jail-free card, even though it is getting a little late for that), dump the others, turn this place around before you wake up to find that you’ve been doing their dirty work, too.

Bean’s ego and bankroll is more important to Gottfredson than quickly demonstrating to the faculty that he understands how far off track UO has gone? I like the plan for performance evaluations. But Bean simply has to go, now. Before he spams us again, please!

Thought-provoking analysis . Coincidentally if people are searching for a IRS 9465-FS , I used a sample version here http://goo.gl/lAiXo6