Subject: deans-dirs: Welcoming Dr. Cassandra Moseley and Dr. Andrew Nelson to the VPRI Office Date: July 2, 2015 Dear Colleagues: We wish to announce that two colleagues are joining our efforts in the Vice President for Research and Innovation office as of July 1, 2015: Dr. Cassandra Moseley as an…

Posts tagged as “Brad Shelton”

2/5/2015 update: A reader passes along this Brad Shelton powerpoint, which among other things documents the $1.5M Moffitt to Moffitt transfer: The bottom line though, is that there’s plenty of water in the well. Or at least that’s what Brad Shelton was telling UO’s academic deans in September: I wonder…

Diane Dietz reports the sad news on Ed Awh and Ed Vogel, two top “cluster of excellence” professors who are leaving UO for the University of Chicago, in the RG here. The report on our newly appointed and overpaid Interim VP for Research Brad Shelton is here. UO Today video…

UO’s overpaid VP for Research Brad Shelton is going to have an interesting time rationalizing these low retention offers. Diane Dietz has the story in the RG, here: At least one UO brain researcher has already been poached. Clifford Kentros, a neuroscientist in the psychology department, who designed and produced…

9/21/2014 update: That may even have been more than the latest increase in the athletics budget. The report from UO’s astonishingly well paid new VP for research Brad Shelton is here. Oregon State has a real-time dashboard showing their data, here. If anyone knows where the full UO report is please put the link in the comments, thanks.

5/20/2013 updated Updated: Beavers crush Ducks in Civil War for research money, with athletic spending number chart, and at the bottom, some salary and consulting payment info from Espy’s office.

Diane Dietz has the story and data on UO here. I got the OSU data from their very complete Research Office data page, here. Both are “Federal Flow Through” totals, which are the easiest to find directly comparable data. They include spending on outreach and instruction, but it’s mostly research money and the trends look similar no matter how you cut it. That’s the table on the left. The table on the right shows athletic department spending, from USAToday. (Official UO and OSU numbers for 2012.)

Oregon is paying VP for Research Brad Shelton (a former UO math prof) $304K to manage UO’s $97M research budget. Four years ago we paid Rich Linton $185K. For comparison, Michigan State is paying Steve Hsu (a former UO physics prof) $277K to manage MSU’s $330M research budget. (Last year’s…

Let’s hope this is the beginning of the end.

5/29/2014: UO Trustees Academic Affairs committee to meet today

Notice: The UO Trustee’s committees will meet On May 29 and June 3, and the full board will meet June 12-13. Info here. Today’s meeting:

12:30 PM, Thursday, May 29, 2014 – Public Meeting – HEDCO Education Building, Room 230T

1.0 Convene

• Call to Order and Welcome (Mary Wilcox)

• Roll Call

Present: Coltrane, Holmes, Geller(!), Thompson, K Willcox, Ford, Shelton, Chapa, Altmann. On the phone: M Willcox, Dotters-Katz, Lillis. No Curry, no Blandy. About 15 in the audience.

President Gottfredson is missing. Odd, it’s on his schedule.

As announced on April 15, Dr. Kimberly Andrews Espy will be leaving the University of Oregon on May 23 to take a new position at the University of Arizona. After consulting with a number of faculty and administration colleagues over the last few weeks, the President and I have made some decisions about how best to transfer the responsibilities of the office for Research, Innovation, and Graduate Education. Beginning Tuesday, May 27, we will separate the responsibilities of Graduate Education from Research and Innovation. Today, we are pleased to be naming two interim positions, both of which will report directly to me.

2/21/2014 update: Speaking of bloat, here’s a nice benefit for money-losing UO basketball coach Dana Altman, to top off his $1.8M salary, bonuses, and “opportunities to earn outside income”:

During the Term of this Agreement while Altman is head men’s basketball coach, and upon presentation of proper receipts, Altman will be eligible to receive up to twenty-five thousand dollars ($25,000) per year to reimburse him for travel expenses incurred by his relatives and friends to attend University athletic events or for the purpose of visiting Altman.

Latest contract here: https://dl.dropboxusercontent.com/u/971644/uomatters/IAC/Altman-2.pdf

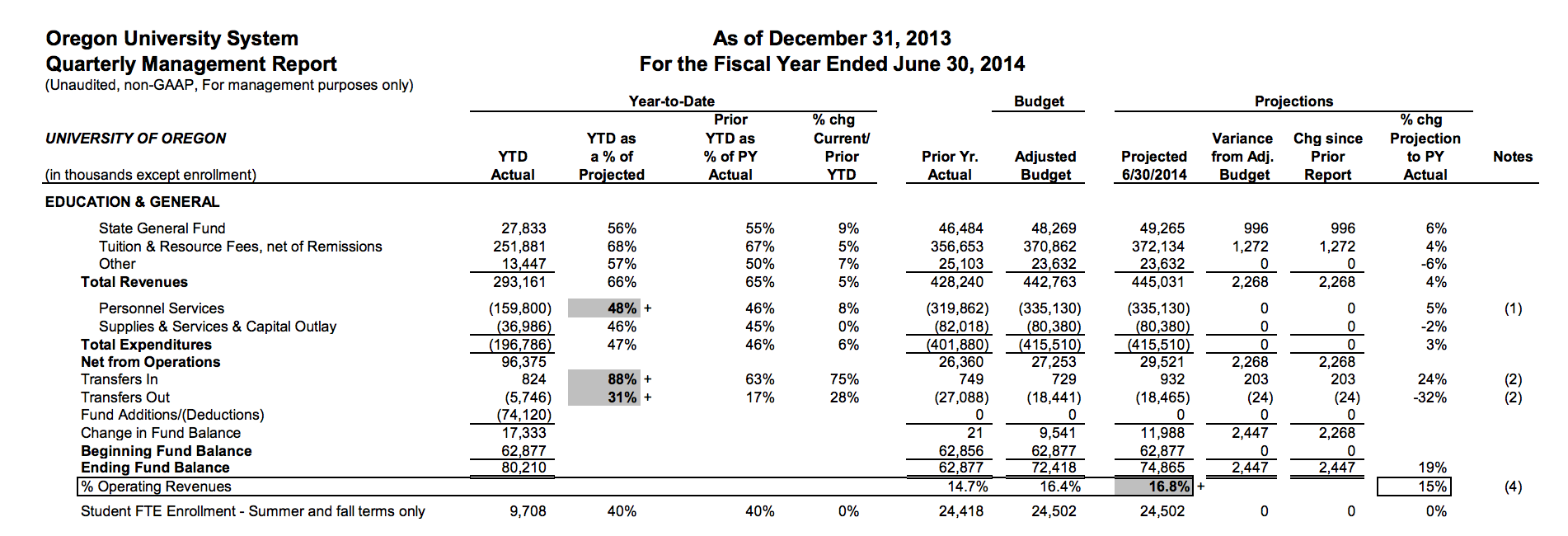

2/20/2014 update:The news from CAS is all about how Brad Shelton’s budget model is going to hold back still more tuition for UO’s central administrators to play with next year. Meanwhile, UO’s latest report to OUS shows that UO’s reserve funds are steadily increasing, by about $12M in just one year according to the forecast. This is after payment of the first round of union raises. The next round starts July 1, and will cost ~$8M, while tuition increases and new state funding will bring in about $18M in new money. So expect further increases in reserves, and more of the same BS from the administrators about “the well is dry”.

2/18/2014: VPFA Jamie Moffitt’s transparent reports reveal administrative bloat

Budget VP Brad Shelton is now hiding his Budget Model reports behind a password wall, presumably in response to me outing Doug Blandy’s $1M AAD 250-252 student credit hour heist. Reminds me of back when Frances Dyke was VPFA and took the excel spreadsheet explaining the accounting codes off her website, claiming it wasn’t a public record.

But new VPFA Jamie Moffitt has put that file back up, along with a plethora of simple summaries showing where Johnson Hall is spending UO’s money, and plenty more detailed spreadsheets. An admirable improvement from the obfuscation we got from her during union bargaining, presumably under orders from Randy Geller. Here are some highlights.

10/31/2012: Today’s message from our interim provost – presumably sent with Gottfredson’s blessing – represents some serious backtracking regarding Brad Shelton’s 2009 “New Budget Model”, of which Shelton wrote: What is RCM? In most modern American universities, authority is highly decentralized, but responsibility (specifically financial responsibility) is held centrally. This decoupling of authority…